Blockchain Explained Like You’re Five (Part I)

Introduction

Blockchain technology is a hot topic, but it’s still early days. In this guide, we’ll explain how blockchain works and why it has the potential to transform business processes.

What is blockchain?

Blockchain is a digital ledger for recording and verifying transactions. It’s a database that is shared across multiple computers, so it can be used to record anything from money transfers to medical records.

The technology behind blockchain was first developed by Satoshi Nakamoto in 2008 as part of the bitcoin cryptocurrency project; however, its application has since expanded far beyond cryptocurrencies into many other industries and areas of life.

To understand how blockchain works, we need to go back to basics:

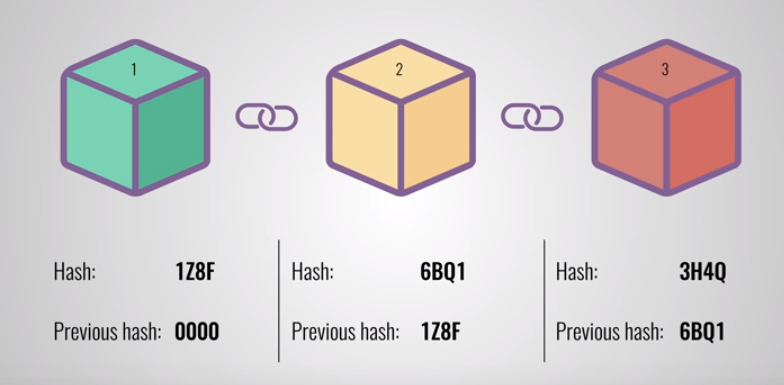

- What is a blockchain? A block (or “link”) contains data about one transaction or event–the date on which it occurred and some details about who created it and why–and then links back up with the previous block using cryptography (encryption). This creates an unbroken chain linking all past transactions together since each new one adds additional security measures against tampering by creating hash values based on previous ones before adding them into their own blocks for future reference purposes

How does blockchain work?

Blockchain is a distributed ledger. It’s made up of blocks, which are transactions. Each block contains a set of transactions that have been validated by the network and then linked together using cryptography (more on this below). The blocks are then linked using hashes, digital signatures and consensus algorithms.

Why is everyone talking about blockchain?

Blockchain is a distributed ledger, meaning that it’s a database spread across multiple computers. Each piece of data in that database is called a “block.” Every block contains information about its previous block, which makes them connected and immutable–meaning they can’t be changed or deleted.

Blockchain technology is also transparent because anyone can see all transactions recorded on the blockchain at any time. This means that no one can hide from their past actions or make false claims about what happened during them (and when).

Another key feature of blockchain technology is decentralization; there’s no central authority controlling how people use it, like banks do with money transfers and credit cards do with payments. Instead, users control their own digital assets by using their private keys (which are just long strings of numbers) as passwords to access their funds through an online wallet service provider like Coinbase or Binance Exchange

Blockchain technology has the potential to transform business processes, but it’s still early days.

When you think about blockchain, you probably picture an impenetrable wall of data. But in reality, it’s much more than that–and much simpler too. Blockchain technology is a distributed ledger system that allows people to record information securely and transparently without the need for a central authority or third party. In other words: Blockchain is a way of recording and sharing information; it’s how we store and share information in a secure and transparent way; it’s also how we store and share information securely, transparently (and efficiently).

Conclusion

Blockchain technology has the potential to transform business processes, but it’s still early days.

In this article, we’ve tried to explain blockchain as simply as possible by using analogies that even a five-year-old could understand. Hopefully this helps you better understand how blockchain works and why it’s so exciting!