Blockchain 101: Explaining Blockchain Technology

Introduction

Blockchain technology is the next big thing, and it’s already revolutionizing the way we transfer data and manage transactions. But what is blockchain? How does it work? And how will it impact the future of technology? In this article, I’ll give you a brief history of blockchain, explain how the Internet of Things (IoT) ties into blockchain and its impact on IoT security ecosystems, and more!

What is blockchain?

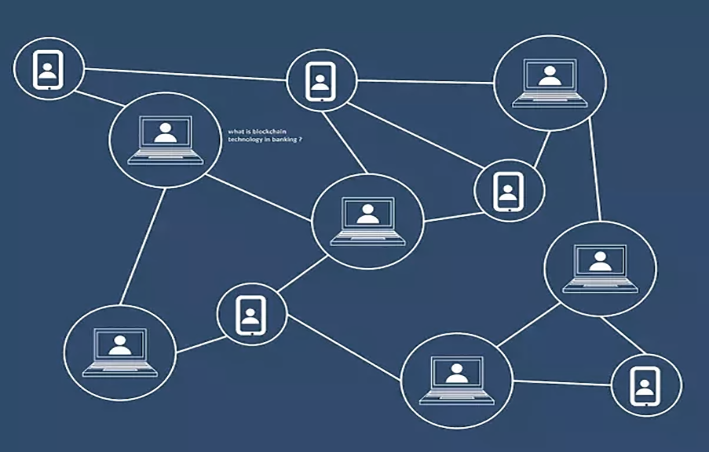

Blockchain is a distributed ledger. It’s a way to transfer data between parties in an efficient, secure and transparent way.

Blockchain technology eliminates the need for third parties like banks or credit card companies by creating a decentralized database that records transactions between two parties efficiently and in a verifiable way.

A brief history of blockchain

Blockchain was created to solve the problem of trust in peer-to-peer transactions. In its simplest form, blockchain is a distributed ledger that maintains a continuously growing list of records, called blocks. Each block contains data and information about transactions, such as transaction time and amount paid or received.

The first recorded use of blockchain was in 2008 when Satoshi Nakamoto (the inventor’s real identity remains unknown) introduced Bitcoin as an alternative digital currency to fiat money issued by governments or central banks. Since then, many other cryptocurrencies have been created using this technology including Ethereum and Litecoin; however Bitcoin remains the most popular cryptocurrency due to its high value per coin ($4K+ USD).

How does the Internet of Things (IoT) tie into blockchain?

The Internet of Things (IoT) is simply the interconnection of devices, vehicles and buildings through internet-enabled technology. It’s a concept that we’ve been hearing about for a while now, but it’s only recently started to come into its own. The IoT has enormous potential–one report estimates that the global market will grow from $656 billion in 2015 to more than $1 trillion by 2020–but there are some major challenges holding back widespread adoption right now.

One of those obstacles is security: how do you keep sensitive information safe if it’s being transmitted across multiple networks? Blockchain could be one solution; as we discussed above, this technology provides an unalterable record of transactions between two parties who don’t know each other personally–and this same principle applies when it comes to securing data from hackers who want access without permission.

Blockchain’s role in the IoT security ecosystem

Blockchain technology is a distributed ledger system that provides a way for data to be tracked and verified. Blockchain can be used to track the movement of physical goods, digital information and cryptocurrencies.

Blockchain has gained popularity in recent years due to its role as the underlying technology behind Bitcoin and other cryptocurrencies. However, blockchain’s potential uses extend far beyond just cryptocurrency transactions: it can also act as an immutable record keeper for many industries including manufacturing, supply chain management, logistics and even healthcare (to name just a few).

Blockchain technology is a new way of transferring data that eliminates the need for third parties.

Blockchain technology is a new way of transferring data that eliminates the need for third parties. A blockchain is a distributed database, meaning it’s stored on multiple computers and isn’t controlled by any single entity. It’s also decentralized, which means no single person or organization has control over it.

A blockchain is essentially a digital public ledger–a shared database that records transactions between two parties efficiently and in a verifiable way. For example, when someone buys something with Bitcoin or Etherium (two types of cryptocurrency), all the other people in the network can see that transaction happen instantaneously thanks to cryptography and consensus algorithms built into their systems’ architecture; this prevents fraud while keeping costs low because there’s no need for middlemen like banks or governments who traditionally handle transactions between buyers and sellers via fiat currencies like dollars or euros today.”

Conclusion

Blockchain is a new way of transferring data that eliminates the need for third parties. It’s a distributed ledger system that allows users to securely store information without relying on a central authority or server. This technology may seem complex at first glance, but it has the potential to transform industries like finance and healthcare by making processes more efficient while ensuring data integrity at every step along the way